Intra-Group Stamp Duty Relief – Recent Court of Appeal’s Judgement in Hong Kong

On 5 July 2024, the Hong Kong Court of Appeal (“CoA”) overturned a judgement made by the Hong Kong District Court (“DC”) regarding stamp duty relief on intra-group transfer of shares of a Hong Kong company pursuant to section 45 of the Stamp Duty Ordinance (“SDO”)1.

Basic facts of the legal case on Intra-Group Stamp Duty Relief

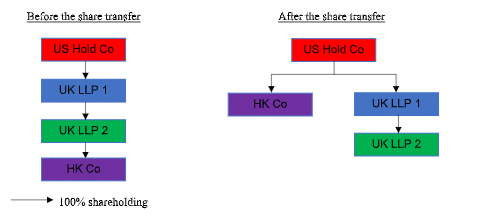

In this legal case, as part of an in internal group restructuring, shares of a Hong Kong company called John Wiley & Sons (HK) Limited (“HK Co”) were transferred from a limited liability partnership registered in the United Kingdom called John Wiley & Sons UK2 LLP (“UK LLP 2”) to a limited liability company established in the United States called Wiley International LLC (“US Hold Co”).

Prior to this share transfer, HK Co was wholly and indirectly owned by US Hold Co through UK LLP 2 and another limited liability partnership registered in the UK called John Wiley & Sons UK LLP (“UK LLP 1”). The shareholding structures before and after the share transfer are depicted as follows:

UK LLP 2 and US Hold Co (collectively referred to as ‘Appellants’) applied for stamp duty relief in respect of the transfer of HK Co’s shares on the ground that the transfer of shares was conducted between ‘associated bodies corporates’ pursuant to section 45 of the SDO.

The key issue was whether US Hold Co, which held indirectly the entire beneficial interests in UK LLP 2 (being a limited liability partnership), could be regarded as the beneficial owner of not less than 90% of the ‘issued share capital’ in UK LLP 2 for the purpose of the stamp duty relief.

Initial ruling by the District Court

The DC considered that the term ‘body corporate’ is a broader term than ‘company’, and the relief should apply to all associated groups, regardless of whether their relevant members were incorporated as companies with limited liability or other forms of bodies corporate.

A body corporate has ‘share capital’ so long as the capital of that body corporate is divided into quantifiable portions and all such shares together make up 100% of the total value of the capital.

UL LLP 1 and UK LLP 2 were considered as having issued share capital (each in the nominal value of GBP 100, having been divided into 2 portions – GBP 1 and GBP 99, which have been taken up and paid for by the initial members) and satisfied the association requirement under section 45 of SDO and hence can be entitled to the relief.

Appeal ruling by the Court of Appeal

The CoA however opted for a narrower interpretation of ‘issued share capital’ and ‘associated body corporates’. The CoA concluded that UK LLP 1 and UK LLP 2 are not ‘companies’ and therefore do not have share capital neither shares issued.

It followed that US Hold Co cannot be the ultimate beneficial owner of not less than 90% of the issued share capital of UK LLP 1 and UK LLP 2. As such, the Appellants failed to satisfy the association requirement under the stamp duty relief.

Our insights on Intra-Group Stamp Duty Relief

Our view is that the original intention of granting the stamp duty relief for intra-group share transfer under section 45 of the SDO may not have been limited to companies with issued share capital, but also to other forms of bodies corporate.

Unfortunately, following the judgement of the CoA, the intra-group stamp duty relief will be restricted to companies with issued share capital only. Meanwhile, let wait and see whether the Appellants will lodge an appeal to the Court of Final Appeal.

How HKWJ Tax Law can help

It will be of utmost importance that corporate structures are crafted carefully in the initial setup and/or the subsequent restructuring for the sake of the potential stamp duty exposures as well as other tax aspects.

One is therefore recommended to obtain professional review and assessment regarding the corporate holding structure. Please feel free to reach out to our team of seasoned tax professionals for a comprehensive advice on the stamp duty and/or other tax matters under your unique situation.

Footnote:

1 Section 45(2) of the SDO stipulates that transfer of a beneficial interest in Hong Kong stock from one associated body corporate to another can be exempt from stamp duty, provided that, amongst others, the two bodies are associated (being one is beneficial owner of not less than 90% of the issued share capital of the other, or a third body is beneficial owner of not less than 90% of the issued share capital of the two bodies.